Date of publication: July 16, 2026 | Estimated time to read: about 7–8 minutes

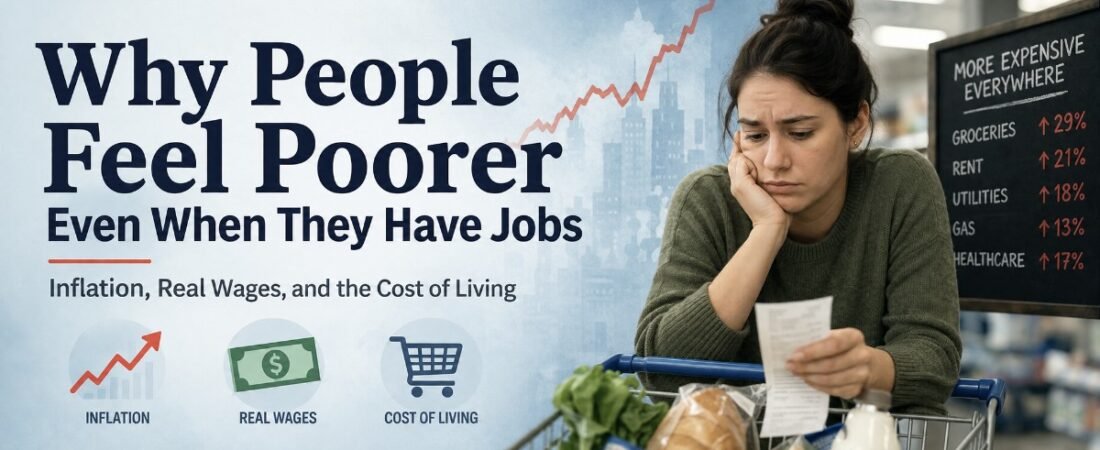

Many people assume that having a job should automatically bring financial comfort, but that is not always true. In today’s economy, it is common for workers to feel poorer even while earning a regular paycheck, because the cost of living has risen faster than their income. Rent, groceries, transport, electricity, debt payments, and other essential expenses can grow so quickly that a salary no longer stretches as far as it once did. As a result, a person may still be employed full-time and yet feel financially squeezed, stressed, and unable to build savings.

This feeling of being poorer is often linked to inflation, which reduces the real value of money over time. Even when wages increase, they may not rise enough to keep up with prices. That means a raise on paper does not always translate into a better life in practice. A worker might earn more than before, but if housing, food, and energy costs rise faster, the extra income disappears before it can improve day-to-day comfort. This is why employment alone does not guarantee financial stability anymore.

Inflation and the Loss of Purchasing Power

Inflation affects workers in a very direct way because it changes what their money can buy. When prices increase, the same salary buys less food, less fuel, less transport, and fewer services than it did before. Even a small annual increase in prices can have a large effect when it continues over many months or years. People often notice this first in their weekly shopping bill or monthly utility costs, where the difference becomes impossible to ignore.

The most important point is that wages are often slower to adjust than prices. A worker may receive a modest salary increase, but if inflation is higher than that increase, their real income has fallen. This is why many people feel that they are working harder without actually improving their standard of living. They are earning money, but the money is losing value at the same time.

Why salary increases do not always help

A pay rise sounds positive, but its effect depends on how fast prices are rising. If inflation is high, a small wage increase may only preserve a worker’s position rather than improve it. In some cases, the raise does not even fully protect purchasing power, so the employee ends up worse off in real terms. This creates frustration because the number on the payslip looks better, but the monthly budget feels tighter.

People also compare their current situation with what they remember from a few years earlier. If the same salary once covered rent, food, savings, and some leisure, but now only covers essentials, the emotional effect is strong. The worker may feel like they are falling behind, even if their career is progressing. That gap between income and lifestyle is one of the clearest reasons people say they feel poorer despite having jobs.

Housing Costs and Daily Pressure

Housing is one of the biggest reasons workers feel financially trapped. Rent and mortgage payments often take the largest share of household income, especially in cities and areas with strong demand. When housing costs rise faster than wages, employees lose flexibility in the rest of their budget. They have less money for savings, travel, family needs, and unexpected expenses.

This pressure is especially hard because housing is not optional. People can reduce some spending on entertainment or luxury items, but they cannot easily avoid paying rent or maintaining a home. Once housing consumes too much income, everything else becomes harder. The result is a constant feeling of strain, even among people who are fully employed and working hard every day.

How housing changes the feeling of wealth

Many workers judge their financial well-being not by salary alone, but by what that salary allows them to do. If most of their income goes to housing, they may still be “earning well” yet feel unable to enjoy life or plan ahead. This can make them feel poorer than they actually are on paper. Over time, rising housing costs can be more damaging to financial confidence than a one-time expense, because they repeat every month.

Housing also affects long-term planning. When people spend too much on rent, they save less for emergencies, retirement, education, or home ownership. That lack of progress creates emotional fatigue. Even if the job is stable, the person may feel stuck, because the paycheck is being absorbed before it can create a better future.

Food, Energy, and Essential Expenses

The cost of food and energy has a strong effect on how people feel about their finances because these are unavoidable daily expenses. When grocery prices rise, families notice immediately. When electricity, gas, or transport costs go up, the pressure is repeated month after month. These are not luxury purchases; they are basic parts of normal life, so any increase creates real discomfort.

People often underestimate how much these small increases matter. A few extra dollars or euros on several essentials each week may not seem dramatic, but over a year the total becomes significant. That gradual squeeze makes households feel like their money is leaking away. The worker still has a job, but the job no longer seems to deliver the level of comfort it once did.

Why essentials shape emotion

Essential expenses are powerful because they affect survival, not just convenience. If food, heating, or transport becomes more expensive, people feel insecure very quickly. They may start changing habits, buying cheaper products, delaying trips, or cutting non-essential spending. This behavior signals a deeper emotional shift: the person no longer feels financially comfortable, even if their employment has not changed.

This is also why inflation becomes a political and social issue. People usually do not talk about economic theory when prices rise. They talk about whether they can afford groceries, gas, or school supplies. In that sense, inflation becomes personal very fast, and the feeling of poverty can spread even in households that are technically employed and earning.

Debt, Taxes, and Take-Home Pay

A job does not automatically mean that all of the salary is available to spend. Taxes, insurance contributions, pension deductions, and debt repayments all reduce take-home pay. Many workers focus on gross salary, but what matters in everyday life is net income. If the net amount is small after deductions, then even a decent salary may not feel sufficient.

Debt makes this worse because it limits freedom. A person who pays credit cards, loans, or mortgage installments every month may have very little left after the fixed obligations are covered. If interest rates rise, those payments can become even heavier. The employee then feels trapped between rising living costs and financial commitments that are difficult to escape.

Why net income matters more

People experience life through the money that actually arrives in their account. Gross income may look strong on a contract or salary announcement, but it does not pay for groceries, rent, or fuel. That is why many workers feel disappointed after a raise that looks meaningful on paper but barely changes the amount they can use. The gap between gross pay and practical spending power is often larger than people expect.

This is one reason economic discussions can feel disconnected from real life. Official figures may show wage growth, but households may still feel pressure because take-home pay has not kept up with costs. When debt and deductions are added, the worker’s effective financial position may remain weak. That is how a person can have employment, steady income, and still feel poor.

Job Security and Financial Stress

Having a job is not the same as feeling secure. Many workers worry about layoffs, contract changes, automation, or a recession. Even if they are employed today, they may not trust that the situation will remain stable tomorrow. That uncertainty changes how they spend, save, and plan. A stable salary is less comforting when the future feels uncertain.

This emotional side matters because financial well-being is not only about numbers. It is also about confidence. If a worker believes that one unexpected event could destroy their budget, they will not feel financially healthy. That is why two people with the same salary can feel very differently about money depending on their debt, family responsibilities, and job stability.

Why insecurity changes behavior

When people feel insecure, they tend to become cautious. They may cut spending, avoid big purchases, and postpone plans for the future. Even if they are not actually unemployed, the fear of losing income can make them behave as if they are already in crisis. This mental pressure contributes to the overall feeling of being poorer, because money starts to feel fragile rather than reliable.

That is why employment alone is not enough to describe a household’s well-being. A strong paycheck helps, but stability, affordability, and predictability matter just as much. If any of those are missing, the worker may still feel financially weak. In practical terms, the problem is not only how much people earn, but how safe and usable that income really is